2024 Annual Letter

Portfolio returns (in €)

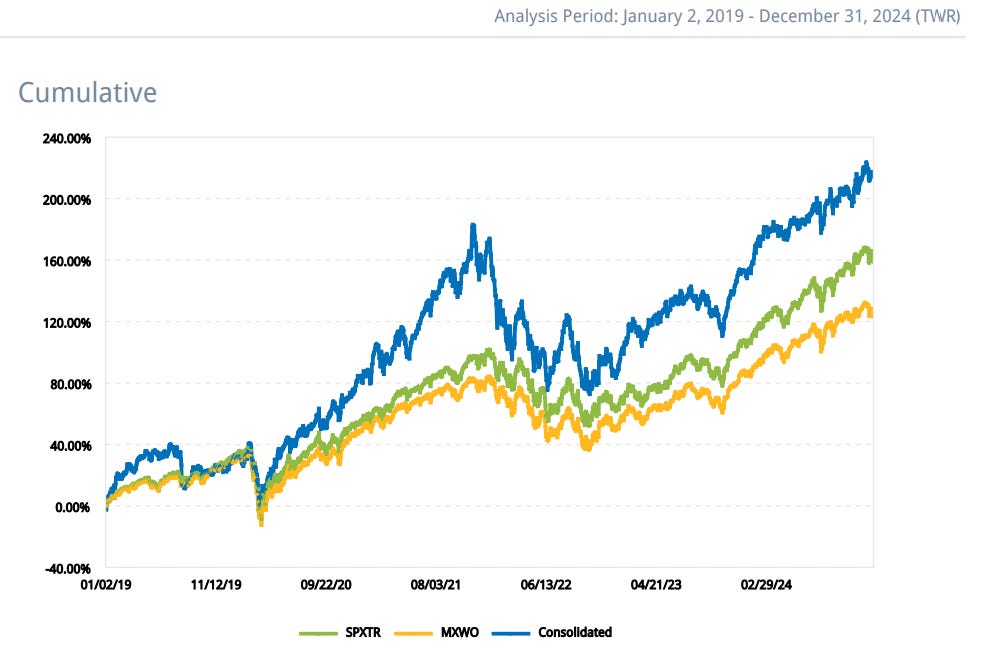

2019: +30.2%

2020: +41.8%

2021: +47.4%

2022: -29.9%

2023: +36.2%

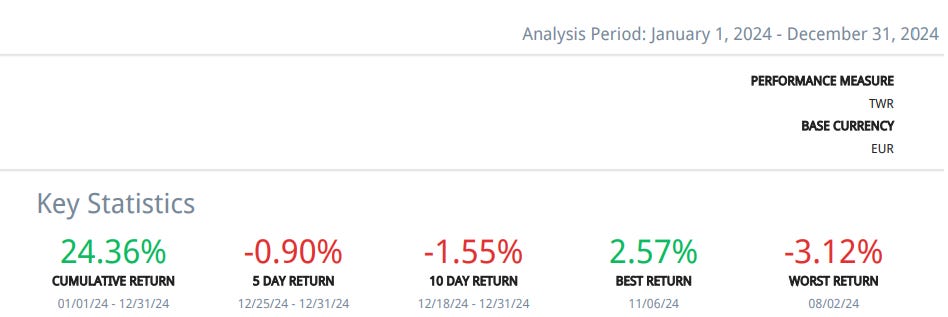

2024 : +24.3%

CAGR 2019 - 2024 (6Y)

Portfolio: +21.0%

S&P 500: +17.1%

MSCI ACWI: +12.7%

I am pleased to be achieving returns exceeding my target (18% CAGR) but, in all fairness, the time for congratulations will come when I have been doing this for at least a decade. The conclusion I can draw from these last 6 years is that, even if this is the right path, I still have a lot to learn. The learning process matters more than any short-term return when you intend to invest for the rest of your life. I think I am doing things better every year, but all these years my returns would have been higher had I not made several mistakes that we could call unforced (we are undoubtedly our own worst enemy). I am not the smartest guy, but I do tend to learn very quickly when it implies losing money. The blog has played a fundamental role in becoming a better investor because I believe that good (long-term) returns are the result of a continuous learning process driven by intellectual curiosity. That is why I am incredibly grateful to all paying subscribers because first (and most importantly) you help pay my family's bills and second, you make me a better investor. I started the blog 4 years ago and not in my wildest dreams did I think I would still be writing this annual letter to so many people who find added value in what I do and how I think. To be honest, I just do the best I can. There are many people out there doing the same thing I do, and I am really grateful that you have decided to be here.

My annual unrealized gains on Interactive Brokers are beginning to exceed the gross annual salary from my main job, and the capital managed represents an increasingly relevant percentage of my family's total wealth. It is amazing how one can make money by reading, reflecting and then making a few clicks – it is the most fascinating game in the world. My dear late grandfather, who worked construction to make ends meet, would have thought I am the luckiest guy ever. In reality, I think that most of us are not grateful or even aware enough of how easy it can be today to bring food home. However, with money comes responsibility and, not gonna lie, it can be a bit daunting when you have a family that depends on you (and a two-year old to boot). At this point, I am convinced that the most important thing for me is not finding the next 100-bagger that some investors seem to be obsessed with – I was too. The most important thing is to have common sense and think about what I can lose before thinking about what I can win. Compound interest is the most powerful force in the universe, but in order to win, you first have to not lose. Fortunes are built by avoiding mistakes that can put you out of the game. Both consistency and the absence of unforced errors are essential if I want to preserve and increase my family's purchasing power for decades to come.

I could be just a couple of clicks away from selling all my positions and building our dream house with hardly any mortgage. My wife is well aware of that, and we would certainly live under less pressure. We opted not to, and delayed that instant gratification. In exchange, in 15 or 20 years, if we continue doing things the way we have done them until now, we will never have to worry about bringing money home or supporting our children if they want to study, start a business or do whatever they like without having to worry about finances. I am very aware that mistakes can distance us from that goal and for that reason I am increasingly strict when it comes to selecting companies to invest in.

Don't get me wrong: I like to invest in good companies, with barriers to entry, tailwinds and led by excellent management teams, but I'm also trying new things. Currently, my so-called “permanent portfolio” is made up of 19 different companies. These have everything I am looking for as true long-term investments. However, there are a whole host of more than 100 companies that I follow closely that do not fit into that permanent portfolio for one reason or another, but I believe they can provide even higher short or medium-term IRR at the right price. They are among my favorite investment opportunities, which usually occur when a company that everyone recognizes as extraordinary experiences temporary problems. That is where one can find the greatest margin of safety (and not when these companies are doing incredibly well). Financial myopia is the best ally of the long-term investor. If you can be flexible and change your mind quickly (but also be patient when the rest are not), you have a good chance of doing better than the market in the long term. I've been experimenting with this new strategy for a relatively short time (Games Workshop is one such example (link)), but so far I feel comfortable with it and I think paying subscribers may find it useful as well. As I told you a few months ago, I will be sharing all my trades in real time with paying subscribers. My intention is not to draw attention to myself or have subscribers copy what I do (please don't do that). The idea is that since the blog is updated once every month, I don't want paying subscribers to wait for weeks to find out what decisions I am making and why. Thank you very much for your continued support.

On another note, I would also like to thank my friend Diego, one of the best private investors I know here in Spain, because he has inspired me to learn about M&A arbitrage. Buffett's partnership letters were also quite inspiring, even though this strategy was not as popular at the time, and regulators paid less attention to mergers and acquisitions. I still have a lot to learn, but in case anyone finds it useful, I will share my trades in the same way I have been doing. I will finance them in the very short term with debt from Interactive Brokers. Our minds are not prepared to understand what one or two additional percentage points of annual returns can mean over 20 or 30 years. However, I think that the risk-reward ratio here is only acceptable when it comes to small deals with no regulatory risks. Most M&A arbitrage opportunities are just not interesting enough to me.

I would also like to point out that, as I get older and family wealth progressively increases, my investment philosophy will become increasingly conservative. This does not necessarily mean that my portfolio turnover will become lower and lower (in fact, it has only increased in recent years), but I do intend to be very strict with capital management and I am unwilling to take risks that could interrupt the power of compound interest. Life is too short to invest in mediocre businesses or trust management teams that still have a lot to prove.

Before getting into the portfolio and the changes that happened this last quarter of 2024, I would like to wish you all a happy 2025. May this new year bring good returns to all of us, but above all, good health and quality time with our loved ones.

*The following content is exclusive to paid subscribers*

Current portfolio and main changes