Portfolio Update - Q1 2024

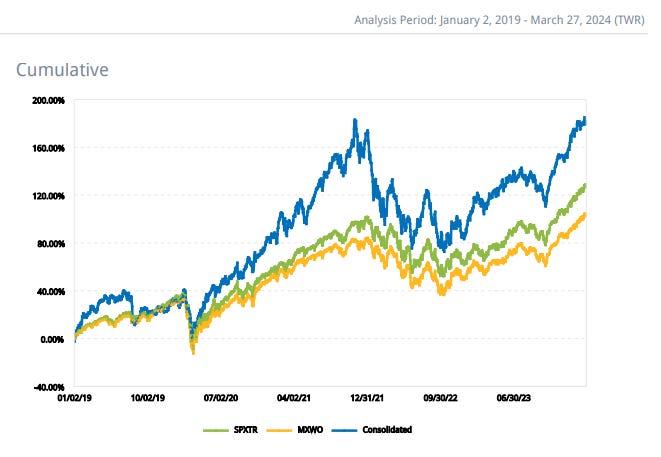

Portfolio returns (in €)

2019: +30.2%

2020: +41.8%

2021: +47.4%

2022: -29.9%

2023: +36.2%

2024 - Q1: +11.6%

CAGR 2019 - 2023 (5Y)

Portfolio: +20.7%

S&P 500: +15.8%

MSCI ACWI: +11.9%

With the portfolio hitting new all-time highs and some stocks exceeding my expectations one would think it is time to make some changes, time to make some decisions. The consensus of investors seems to be that the right thing to do now would be to reduce exposure to companies that have performed well in order to buy more of those that have underperformed because in theory, sooner or later, things usually revert to the mean (for better and for worse). Not only do I not agree with many of the modern theories of “optimal” portfolio management, but I also believe that they can be counterproductive to obtaining reasonably good long-term returns. The truth is that while many companies defy mean reversion, others trade at lower multiples because they actually deserve to. I believe that getting rid of what has worked just because it is trading at high multiples to reinvest capital in lower quality businesses for the simple fact that they are – in theory – cheaper, can only lead to very costly forced errors in the long term.

People often talk about how important it is to have the necessary mental strength to withstand stock price volatility, especially when companies are going through temporary problems. However, not many talk about how, if you have what it takes to hold an investment for many years while enjoying compound interest, there will be periods when the stock will be “optically” expensive. The discipline to do nothing should be the same. A single good investment can change your life as long as you do not systematically sell stocks along the way. Is the stock likely to underperform in the short term if it has previously performed extremely well? It is possible, but making decisions based on market expectations for the coming quarters is not on my roadmap.

Can you imagine telling your family, who has been running a successful bakery for more than three generations, to sell part of the business because last year was too good to be repeated? After all, it can only get worse, right? The reality is that many winning businesses have everything in their favor to remain that way. The reality is that management teams that know how to create value for their customers, employees and shareholders will usually surprise you on the upside. The reality is that speculating on market expectations can only lead to worse results than investing for the long term and making decisions that are solely based on business fundamentals. The ability to pick winners and, more importantly, the discipline to hold onto them for many years is an art. Only investors who are patient enough and think exponentially rather than linearly will build fortunes.

Many of the companies I have been investing in for years may seem expensive, but time always ends up proving the opposite. In my way of understanding investment, the margin of safety has nothing to do with a FCF multiple, but with the quality of the underlying business and the management team's ability to reinvest capital at high returns. There will always be a place in my portfolio for management teams that resist the temptation of pleasing short-termist investors. Of course valuation matters – as time will show sooner or later – but I think trying to do a proper valuation analysis of a business is about a lot more than simply putting a multiple on its earnings.

This quarter marks my sixth year as a Constellation Software shareholder, and I believe it is a perfect example of what I am looking for when investing and preserving family wealth. Additionally, I want to talk briefly about the sales I have made during these first three months of the year. During the first quarter of 2024 there has been more portfolio turnover than I would ideally like, but I am still trying to build a concentrated portfolio with the goal of reducing the number of positions to 20 (now at 26). As usual, below I am sharing with paying subscribers what I have sold and why, as well as where I have reinvested that capital with the goal of generating long-term double-digit returns. Incredible as it may seem, there are still high-quality businesses trading at 17 times 2024 FCF.

*The following content is exclusive to paid subscribers*