Portfolio Update - 05/09/2022

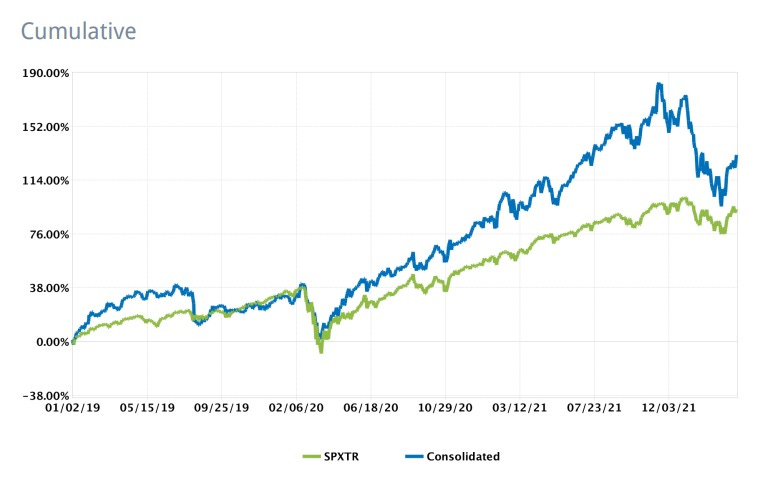

Portfolio returns (in €)

2019: +30.2%

2020: +41.8%

2021: +47.4%

2022 YTD – Q1: -14.8%

Sorry to disappoint, but I am not going to excuse myself with the war in Ukraine, the rise in interest rates or hyperinflation as the main factors that have weighed on the portfolio's return in the first quarter of the year. Good long-term returns are a result of a continuous process of studying and learning, motivated by an intellectual curiosity that will make anyone a better investor. For that reason, I prefer to ignore any macroeconomic event or, in general, factor that is not under my control, and always remain focused on the process rather than on the outcome – and that is what I do want to write about today.

Don't get me wrong – my approach is not superior to any other. Mine has always been an approach that has worked well for me and suits my mental and emotional skills.

I only invest in assets based on their estimated productivity or ability to produce long-term profits, and I only choose those that I will feel comfortable owning for a decade. This approach acts as a first filter and helps me focus only on quality businesses whose competitive advantages will defend their unit economics over time. The perspective of investing thinking in “decades” makes mediocre businesses seem more expensive and exceptional ones seem much more attractively priced. For that reason, I don't invest in businesses simply with valuation in mind because, in quality businesses, time is a structural tailwind. In a way, I try to replicate the culture of many of the companies in my portfolio, acquiring assets with no particular interest in how the market will value those assets in the short or medium term with the aim of making a quick buck. I seek to invest in exceptional businesses, led by management teams that think and act in favor of creating long-term value without falling for the siren songs of a short-sighted market. More than an investor, I like to think of myself as a collector of businesses carefully built not just to grow for the sake of it, but to last.

In the same way, no matter how flashy an investment idea may seem, it's important to first focus on what could go wrong. The real risk is not uncertainty, but the possibility of permanent capital loss. Recklessness is what ends up making the difference in the long term between disciplined investors who trust the process and those who get carried away by trends. The ultimate goal is to invest capital that is irreplaceable (savings from family and friends) and invest it in businesses with competitive advantages that make them difficult to replicate.