Portfolio Update - 10/25/2021

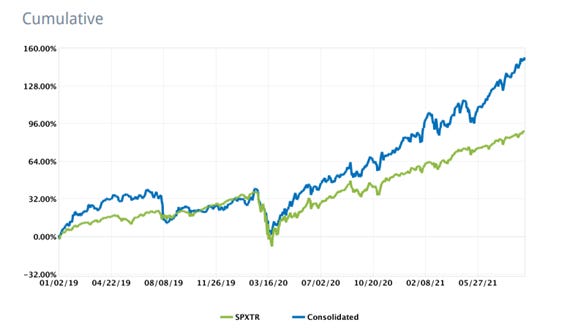

Portfolio returns (in €)

2019: +30.2%

2020: +41.8%

2021 YTD – Q3: +31.5%

Some thoughts about portfolio construction

If investing is more art than science, portfolio construction is the mother of all arts. I haven’t found any piece of reading that perfectly reflects my way of understanding this topic yet, and I’d dare to say I will never find it (perhaps because there’s no perfect one). There are many investment styles, indeed, and some of my friends share this interest in companies with high-quality attributes to try and outperform the market, but none of us deal with portfolio construction in the same way.

When looking at how diverse my portfolio is, you may first think that I’m crazy. The truth is that this thought has always fascinated me. I think what really matters is the returns over the long term – how you achieve them is up to you. I have always found it interesting how taking big bets has usually been regarded as something positive unlike greater diversification, when they are simply two different strategies to face the same game. I guess some quotes from Charlie Munger have been applied literally...

In April 2020 I decided to sell some stocks to build a more robust portfolio that would help me face the coming years. Market uncertainty was at an all-time high then, and nobody knew what was going to happen with the world from then on. Building a more or less balanced portfolio was my way of dealing with such an unknown variable. Despite the fact that the top ten holdings now make up almost half of my portfolio, diversification still makes a lot of sense to me. All the companies in my portfolio could be in the top five at the right price. Assuming that many companies are not at the right price to generate outstanding IRR, keeping them in my portfolio forces me to keep track of them and have some homework ready to capitalize on in times of market stress. If I hadn’t done my homework in April 2020, I would have left great investment opportunities behind (market noise worsens m work quality and slows down my pace). On the other hand, this constant monitoring often leads me to questions that I would have never reached if I hadn’t followed this work methodology. One could say that I am a person who has no interest in a specific football game until I have to bet $10 for the wining team.

Having a reasonable diversification strategy lets me use some cheap leverage at certain times and it also helps me deal with drawdowns when one of the stocks goes through a temporary downturn, because no matter how robust the company moat is or how strong corporate culture is, at some point it will experience some kind of trouble. In the past, taking big bets turned out to be more of a distracting strategy than a tool to boost results for me. It is not easy to keep your composure when your greatest conviction idea weighs down 10% of your entire wealth in a matter of a couple of days. That time wasted worrying about things that I cannot control – that are alien to me – I could have used it to continue analyzing and studying some other companies in my circle of interest. My goal is not to try to hit a home run – I just to try to finish a game that you can enjoy for decades if you can survive on the field.