Portfolio Update - 10/17/2022

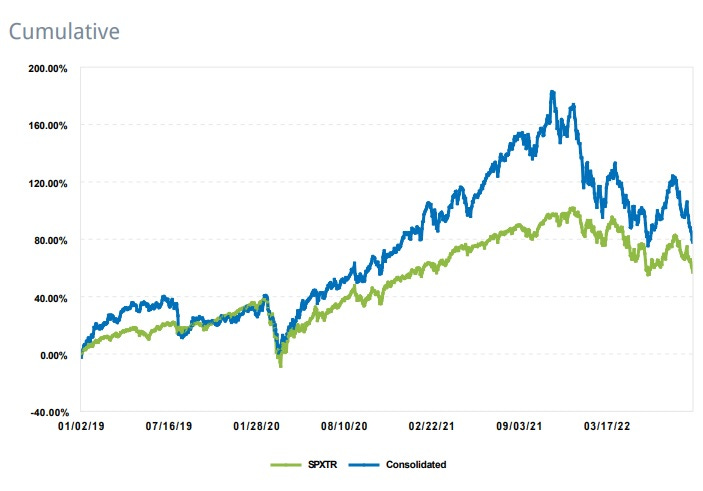

Portfolio returns (in €)

2019: +30.2%

2020: +41.8%

2021: +47.4%

2022 YTD - Q3: -31.5%

"Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas."

Paul Samuelson

Bear markets should not be a reason to panic. In times of volatility, I think it's important to go back to basic investment principles. Short-term price randomness can cloud long-term value growth, depriving investors of building great wealth by thinking with their hearts instead of their heads. Great wealth is built at times like these - it just takes us 10 to 15 years to realize it.

YTD performance isn’t looking good lately, but what is exactly the problem if the companies in my portfolio continue to grow earnings at single or double-digit rates and they are valued at a lower multiple by the market? Somebody who can invest part of their salary every month in unique and irreplicable assets should be able to savor these times.

The real challenge for me is to stay still in a world that is fast changing and full of alarming headlines. Some of my best investments, such as Constellation Software or Xpel, didn’t happen because I invested at the right time, but because I was able to do little even when doing more seemed to make sense. Looking back, I can say that my best investments were a result of buying and not doing much for years. Stock picking is obviously important, but knowing what you're investing in is just as important as keeping your cool when everyone else seems to be losing it.

In the face of mediocre short-term results, it’s easy to think that it’s time to try something different and make substantial changes in the strategy because, at first glance, the current one doesn’t seem to be working. Activity feeds our ego and makes us think that we’re sheltered from failure. Action bias can cause people who are doing the right thing and rowing in the right direction to go on and do the wrong thing, taking them further away from their initial goal. Activity makes us convinced that, in the face of temporary bad results, we at least tried to do something, although on many occasions doing little or nothing would have been much more productive. In investing among other fields, inactivity seems to be some kind of deadly sin.

My discipline and my professional situation allow me the flexibility to act only when it’s reasonable to do so, and not simply because I feel that something needs to be done. During the third quarter of the year, I have continued to gather information before making important decisions and to focus capital on the best ideas in the portfolio. Although the market is indiscriminately punishing almost all companies equally, I still believe that I’m building the portfolio I have felt most comfortable with in my time as an investor. I’m convinced that several years from now, the analytical and psychological effort will be rewarded with great results.

“We don't look at the stock price, it's our culture”

Philippe Maubert, Chairman of Robertet

* The following content is exclusive for paid subscribers *