RCI Hospitality (RICK)

RCI Hospitality may be one of the most interesting companies among those who benefit from the reopening economy.

RCI has two distinct operating segments. On the one hand, the company owns 38 leading cabarets in the US, located in large metropolitan areas, such as New York, Miami, Chicago and Houston (~ 80% of total revenue with normalized EBIT margins above 34%). On the other hand, RCI also owns the Bombshells concept, 10 sports and military themed bars / restaurants located in Texas (~ 20% of remaining revenue with EBIT margins exceeding 24%).

RCI is special for its quality assets and the interesting unit economics of the two business branches. 80% of the generated cash flows come from assets with characteristics typical of local monopolies in a market with a highly controlled supply. The fixed cost structure of these assets is allowing RCI to convert all post-covid demand into profits with sky-high incremental margins. The FCF margin could exceed 25% of 2021 revenue and there are many opportunities to reinvest that capital at rates that could exceed 25% - 30%. RCI CEO, who has been in the role for more than two decades, owns 8% of the company and aims to grow the FCF per share in the next few years to double digits. If the organic growth of April and May is maintained during the rest of 2021, RCI could be trading at a FCF yield of between 11% and 13%.

Gentlemen’s Club operating segment

Rick’s Cabaret, Scarlett’s, Tootsie’s Cabaret or Jaguars Club are some of the 38 clubs that RCI owns and manages. Although most of the clubs are geared towards gentlemen of middle or upper social class, the diversification of styles allows it to cater to a very diverse demographic.

These gentlemen’s clubs can't compete with many restaurants in the quality of their food (10% of total revenue), but their unit economics are significantly better than the most popular restaurant in town. The gross margins of RCI cabarets are around 90% thanks to the sale of alcoholic beverages (38% of total sales) and entertainment services (46% of total sales) whose respective gross margins are 80% and 99%.

In a distraction-laden environment, it doesn't matter much to the consumer that most drinks are generic versions of leading brands, which sell for $10 despite costing only $2 to serve. In most clubs it is mandatory to have one or two drinks to be able to sit down.

These clubs have a fixed cost structure. Once these costs are covered, the additional sales generated go directly to the bottom of the income statement. Around 70 - 80% of this fixed cost structure is covered by selling food, beverages, cigarettes and commemorative accessories or accessories. The key to the business is the revenue from entertainment services and fees from ATMs, which make up 100% of the segment's EBITDA.

Entertainment services provide incremental profits with no added costs for a variety of reasons. Policies in markets where RCI operates do not consider entertainers as employees, but as independent agents who go to strip clubs to offer private or group dances. It is the clientele who pay the dancer's salary (services + tips) and not the club itself.

As if that was not enough, the club charges a kind of entrance fee or rent to the dancers before any performance. This transaction takes place in exchange for providing a themed and safe environment (security personnel work on payroll for the club) and offering a larger customer base than a dancer could get off the premises. In addition, for each dance, either at the consumer's table ($20 - $30 for 1 or 2 songs + tips) or in VIP rooms, the club charges a fee of what the entertainer generates during the dance. The conditions of the fees are negotiated separately with each dancer (depending on her reputation and popularity), but sources from other gentlemen’s clubs outside RCI confirm they can range from 20% to 50%. In some clubs it is also very common for entertainers to have to generate a minimum number of drinks per night. Although it is the dancers who set their own schedules, a normal day can reach 8 hours, in which they could take home $ 1,000 net of fees (pre-COVID).

To avoid the possible fraud of dancers not paying the cabarets, some clubs choose to have a different fee structure and decide to significantly increase the admission fee or rent the dancers must pay before performing. In return, tips are left exclusively to the dancers. RCI is the US strip club market leader and can reduce this risk of fraud by having the largest dancers database in the industry. The entertainers know that a good reputation is key to accessing the most popular cabarets (those that generate the highest consumption per customer).

Another revenue with incremental margins close to 100% is admission fees. In a pre-pandemic scenario, those could range from $20 to $50 depending on the event, day and the time of arrival (the closer to closing time, and therefore, the fewer hours of consumption estimated, the more expensive the entrance could be). This pricing power could be enhanced depending on the demand for the night in question. With the fixed cost structure already covered, other source of income with hardly any incremental cost is the VIP room reservation. Depending on the number of attendees and the services requested, package prices usually range from $400 to $4,000 per night.

Another source of revenue with high cash conversion rate are the commissions generated by the ATM machines. The digitization of payments is reducing the usage of cash in every sector but this one. Clubs allow customers to pay for food and drinks with credit / debit cards, but entertainment services and tips must be paid in cash (> 50% of average consumption per customer). The cost of ATM machines can be around $2,000 - $3,000, they do not need labor, the cost of installation and maintenance is superfluous and they have 24/7 support. The presence of these ATM not only drives consumption in the club, but also generates commissions for the club owner that can go up to $8 - $12 for withdrawals greater than $100 due to the lack of alternatives for the customer. Only a small part of the commissions generated are for the bank accessing an ATM outside its network and for the company processing the operation. Most are for the ATM owner (the club owner).

Due to revenue quality and cost structure flexibility, the EBIT margin of this operating segment was 26.8% in 2020, with half of the establishments closed due to COVID, capacity limitations for those open, without being able to charge entry fees and with completely depressed revenue for entertainment services. Pre-COVID EBIT margins were 35.9% and 35.1% excluding one-off non-operating expenses.

Disclaimer: Please, note that some prices are estimations and may not correspond to those of RCI. The author has tried to adjust the numbers as closely as possible after interviewing a couple of US small strip clubs owners. RCI does not provide any breakdown on their commissions or services.

Gentlemen’s clubs have attractive unit economics, but are they sustainable for the coming decade?

RCI's clubs are small local monopolies that don't run on fads, like nightclubs or bars. The benchmark gentlemen’s clubs of 20 years ago continue to be the same today. This is mainly because, although existing operating licenses are usually protected, the number of new operating licenses granted by governments for new establishments are very small. Municipalities ordinances are very strict with the adult entertainment industry and many operating licenses are subject to fixed city locations. These regulations seek to protect communities and promote law and order, since it is often said that these establishments come with negative side effects (drugs, prostitution, sale of alcohol to minors and other criminal activities).

Governments do not grant new operating licenses before they have knowledge of the planned location of the club. In many counties, strip clubs must maintain a minimum safety distance of 500 feet from any school, residential area, church or religious institution, park, public work or area frequented by minors. Also in many counties, cabarets have to maintain a minimum distance of 1500 feet between one another, as governments are concerned that the side effects of these establishments can be enhanced by having several of them in the same area. In towns where land available is scarce, many governments deny permits for the construction of new clubs even when requirements are met. They are aware that opening a new gentlemen’s clubs limits the interest of future contractors and the viability of new public work projects.

If, even with these limitations and after the bureaucratic delay these applications entail, a license for new construction was issued, the gentlemen’s club would also have to obtain a license to sell alcohol to its customers (those are two independent licenses). If this second license was denied, the ROIC of the club would not be attractive enough to continue with the project (due to the specifics of the cost structure of this business model).

On the other hand, the regulations on the use of advertising to attract customers are also very restrictive. As a general rule, direct advertising of any kind are not allowed on the windows, façade or surroundings, except for the specific areas marked by law. In addition, unlike the entertainment sector for all audiences, cabarets cannot benefit from free advertising by consumers on social media. These platforms restrict content that has anything to do with partial or full nudity. As with tobacco companies, such restrictions strengthen established players with reputations behind them.

Another equally interesting aspect is the restrictions on capacity expansion for existing establishments. Even indoors, regulations are very specific about the arrangement of the different elements. Modifications must be purely aesthetic. These regulations serve as a natural protection for the industry. Possible capacity expansions in certain markets are limited, preventing supply from being overloaded. Advertising restrictions and maintenance capex not only increase barriers to entry, but improve ROIC for clubs.

All these factors turn RCI’s clubs into local monopolies with very strong entry barriers. RCI itself has built 80% of its national gentlemen’s club network through M&A.

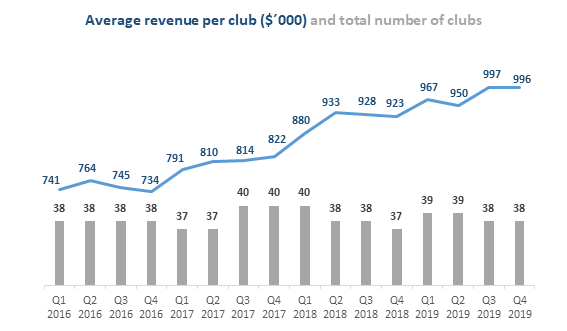

Cabarets tend to do better during booming business cycles. In recent years, increased consumer confidence and per capita spending have improved customer traffic. Furthermore, the competitive position has allowed RCI to exploit its pricing power in some of its services. Both factors have increased the organic growth of cabarets by 10.3% CAGR since 2016 until before the pandemic broke out.

Source: Author using company filings

Bombshells operating segment

RCI also operates sports and military themed bars / restaurants in Texas. With 8,000 sq. ft. indoors and over 1,900 sq. ft. outdoors, Bombshells is a concept with a larger scope than traditional sports bars. Out of the 10 existing Bombshells, 8 are located in Houston, the fourth most populous city in the United States, with 2.3 million inhabitants and where people dine out an average of 7 times a week compared to 5.9 in the national average. The first Bombshells was opened in 2013, and now there are 10 and 3 more are being developed, the goal being opening 100 of them in the next 10 years (80% franchises, 20% owned).

The Bombshells concept is interesting for a number of reasons. Although the main attraction is the waitresses who wear military uniforms, Bombshells is a less niche place than Twin Peaks and Hooters, which focus their theme on a purely male clientele. According to the management, 70% - 80% of the Bombshells customer base is completely different from these two concepts. Men, women, families, singles and couples come to Bombshells to enjoy food, drink and, above all, entertainment (more than 40 TVs per restaurant, DJs and frequent events). Bombshells is open until after midnight and those hours before closing are the most important of the day. The average customer who attends before late night is a male / female customer between 25 - 35 years old accompanied by a group of friends. The atmosphere created at night triggers per capita consumption and prevents customers from turning to restaurants in the same area to continue drinking and eating. Twin Peaks and Hooters have a different revenue mix. Beverage sales generate higher gross margin and 2/3 of Bombshells revenue comes from this category, unlike the previous two. Contrary to gentlemen’s clubs where the customer can spend $2,000 a night in the premises, the average per capita spending is lower and the concept is designed to handle the largest volume of orders possible. To stand out in such a competitive sector, serving good food is not enough - you have to entertain people.

The board of directors has accelerated the learning curve in recent years. The last two restaurants are getting better ROICs than the first projects thanks to an improvement in customer traffic. The location of new projects is key to driving organic growth and ending up obtaining better operating margins. At first they wanted Bombshells to be well connected to the city, but later they realized that Bombshells did better in places with higher customer traffic. In fact, they perform better when there is more competition / consumer alternatives within the same area.

Although acquiring prime locations implies a higher initial investment (Bombshells own land in most projects), construction costs end up being identical to those in less preferable areas. But it is this variable that determines that the last Bombshells are generating between $100k - $140k a week ($5 million - $7 million a year) compared to the first projects, which used to generate $80k - $90k a week ($4 million - $4.5 million a year).

In the same way that the competition adds value, Bombshells also have a positive impact on adjacent stores traffic. The management, which use bank financing for the projects (the last one was at 3.99% with 20-year amortization), buys lots of land that later clears and sells for future projects that they estimate will favor customer traffic for Bombshells. In one of the last projects of 2020, they acquired land at $9 a square foot and, after the construction of the restaurant, they sold their excess land in two operations, at $16 and $18 a square foot.

Bombshells unit economics have nothing to envy those of McDonald’s or Starbucks franchises. With double-digit organic growth and an EBIT margin of over 24%, the latest Bombshells are making close to $1.5 million annual EBIT. Raising a project of this type requires between $3 million and $6 million depending on whether the land is leased or acquired. After selling the remaining land, RCI can recover 1/3 of the investment, so the ROIC before taxes reaches 35% - 50% depending on the type of operation (purchase or lease).

With the money from the sale of unneeded land they can: (1) pay off debt, skyrocket returns on invested capital and accelerate payback or (2) reinvest in future Bombshells and obtain equally attractive incremental returns. Future Bombshells can finance themselves.

Reinvestment opportunities

RCI’s clubs generate FCF they cannot organically reinvest due to regulatory constraints, but there are still many opportunities to reinvest inorganically and obtain attractive cash on cash returns. RCI is the leader in the adult entertainment industry, but its market share does not exceed 2%. Although the dynamics of the sector tend towards the consolidation of the offer, the truth is that it is still very fragmented. The company has built its network of cabarets through M&A and they expect to keep making more acquisitions each year. In the US there are more than 2,200 cabarets and the management believes that 500 meet the criteria to be acquired (located in cities with population growth, low unemployment rate and high per capita consumption).

RCI acquires and integrates gentlemen’s clubs to its national network at a price of 3x - 4x EBITDA and purchases related real estate at market value. They get cash on cash return of 25% - 33% (pre synergies) for local monopoly licenses that have been, in most cases, in force for more than two decades. RCI is reinvesting at attractive rates due to the lack of competition in purchase bids. More than 80% of the strip clubs in the US are family businesses. Eric Langan, RCI CEO, started this business at 21 when others were 40. Now that he is 50, much of the competition is mapping out their succession plan. The world of nightly entertainment for adults is a complicated industry where owners constantly have to deal with problems that jeopardize the force of the club’s license. The stigma in today's society has undermined the glamor it used to have in the 80s and 90s. An owner of a small club in the US told me about this problem. This owner had inherited the business after the death of his parents, and he noted that many small owners are forced to lie in their day-to-day lives regarding their profession and many ruled out the idea that their children inherit the business. They’d prefer to sell it and let their children decide what to do with a couple of million dollars in their bank accounts.

That is where RCI appears, the best-capitalized player to finance these successions. Common operations involve an upfront cash payment of at least 50% - 60% of the total operation value. Selling party usually has an interest in involving the real state asset together with the license, which increases the amount the purchasing party must pay. A medium-sized club can generate between $1 million and $1.5 million in annual EBITDA, which, added to the price of the real state, could represent an operation of between $5 and $10 million. Given that the industry is made up of small owners players, it is difficult for them to be able to pay 2/3 of the total amount upfront when banks do not usually participate in financing in these markets. In addition, the management assures that they have recently been contacted by some owners of several club chains with the goal of selling their establishments. The transaction could involve a cash upfront of between $20 and $30 million. Scale matters and RCI does not have to compete with private equity, as they have no special interest in investing capital in sectors that can generate reputational problems.

RCI also has opportunities to reinvest achieving high ROIICs with Bombshells. They are working to build a national network of 80-100 restaurants in the next 5-10 years with the intention of franchising 80% of them. This decision has both advantages and disadvantages. Franchising allows for an infinite ROE, reduces capital intensity and improves the scalability of Bombshells. On the other hand, assuming that RCI collects a 5% royalty on the franchised restaurant's sales, the franchise would contribute an annual EBIT of $350K compared to the $1.5 million of a Bombshells under ownership. However, although the ROIC of a Bombshells exceeds 35%, the payback is not enough to sustain the pace at which they want to build new restaurants. The scalability of the concept would be much slower, it could deteriorate before reaching the 100 target restaurants and the capital requirements and the difficulty of managing human resources are much greater.

RCI has recruited Shannon Glaser, with more than 15 years of experience franchising similar restaurants, to carry out the expansion of the Bombshells franchise. In her last job, Ms. Glaser was Senior Director and development project of the Twin Peaks franchise (closest competitor to Bombshells). During the six and a half years she worked there, Shannon Glaser and her team secured more than 120 new franchise deals.

However, the management has already drawn up a plan to build 10 new Bombshells over the next 3 years. Additionally, COVID has improved the ROIC prospects for future projects. Many restaurants in Texas have not survived the pandemic and there is more real state available than before. Not only are they getting better locations, but the cost is lower than two years ago. Interest in the franchise has also skyrocketed now that they have surpassed $50 million in annual sales. RCI has already signed its first franchisee to open 3 new restaurants and is processing more applications following the signing of the first agreement. The management estimates that even with 300 Bombshells built throughout the US the market would not be flooded.

Valuation seems attractive

Currently, gentlemen’s clubs seem to confirm that the return of the famous 1920s is a very real possibility. In the first three months of the year, the cabaret segment posted revenues of $30.8 million, down - 18.7% compared to the same period in 2019. RCI achieved these results with only 29 of the 38 clubs operating most of the quarter.

Although numbers are yet to be published, the management announced in the last earnings call that in the months of April and May they achieved the best numbers in recent years. Even with capacity limitations in some clubs, RCI has earned more than $4.5 million a week from this operating segment. There is, indeed, a certain seasonality, but if they managed to make $220 - $230 million in annual revenue, it would imply an organic growth close to 50% compared to the $149 million in 2019. With the fixed cost structure already covered, great part of the growth would go directly to FCF. Maintenance needs are relatively low in both operating segments (2 - 3% of revenues) and net working capital is positive (customers pay on site or even before enjoying the service) so the conversion of EBITDA into FCF is optimal (55 - 60%). With $220 - $230 million of revenue in an operating segment with EBITDA margins of 39% (pre-pandemic), by the beginning of 2022 RCI could be generating between $55 million - $60 million of FCF only with the cabaret branch, without assuming an expansion of margins or an improvement in cash conversion. Moreover, Bombshells is making between $13 - $15 million in revenue per quarter with EBIT margins between 24% and 30%. Assuming an EBIT margin of 24%, that's about $14 million of EBIT or $10 million of FCF for this year. A total of $70 million of FCF between the two business segments would almost triple what the consensus of analysts expects for this year. If RCI keeps up the pace with share buybacks, the company may be generating $8 per FCF share by 2021 - early 2022. The company could be trading at $62 per share or 7.7x FCF in an ideal scenario. A 13% FCF yield for a company with local monopolies, pricing power, few maintenance needs and the ability to reinvest free cash flows for many years in opportunities where they are obtaining cash on cash returns above 30%.

Positive optionality but not without risks

Valuation is interesting because it seems not to include the company’s positive optionality. With close to $70 million in FCF, they are now eligible to make acquisitions of cabaret chains that could bring in between $10 - $15 million in annual EBITDA. In addition, it seems that the market is valuing Bombshells as if it were a dead concept when, with the 10 new openings before 2024, this branch could be earning over $120 million in sales per year only by self-managed stores. Each franchise that manages to close could contribute between $350K - $500K of EBIT depending on the royalty that they agree to.

My goal is not to assess what multiple should be paid by the market for this kind of business. I think both shareholders and the management should not spend too much time on this issue. ESG institutional capital is not interested in the stock and shares may have a permanent discount due to the nature of the business. Still, as Eric Langan and his team continue to handle the situation, the market will end up recognizing their work sooner or later (as it always does). In any case, although the company's high cost of capital is limiting in certain matters, RCI can take advantage of it because they are systematic repurchasers of shares (they have bought back 12.5% of total shares since 2015).

Multiple expansion would benefit both short and long-term shareholders equally. RCI could use shares as part of the financing to acquire high-quality cabarets. The owners of these assets with first-class locations would diversify the geographic risk by participating in a company with national revenue. In addition, this type of operation could help them defer paying taxes. A reasonable valuation of RCI's stock would open more doors for M&A.

Still, investors should be aware that certain risks should be considered. In some US counties there has been pressure for dancers to be recognized as cabaret employees. The change in regulations could deteriorate the ROIC of the sector. It remains to be seen if RCI could mitigate part of this contingency by increasing the fees charged to dancers. As long as the cabaret continues to provide an exponentially larger clientele than a dancer could get on her own, it looks like the business model should be able to adapt slightly to a change in regulation.

The late-night adult entertainment industry is often in the public eye for violent fights between customers, sale of alcohol to minors or other illegal activities. The company knows the importance of maintaining order so as not to compromise licenses that have to be renewed annually. Some communities have rallied against the cabarets in the area, although different studies have been carried out that do not correlate the existence of cabarets with the incidence of crime. Although a percentage of the population is against these businesses, the demand has remained stable during the last 3 decades suggesting that the customer base may regard the service as something cultural. A 1992 National Health and Social Life survey already suggested that 17 million Americans attended cabarets at least once a year. In a 1997 article in the U.S. Eric Schlosser's News and World Report reported that by then Americans were already spending more on cabarets than on Broadway, non-profit shows, opera, ballet, jazz, and other classical performances combined. As long as the demand is latent and the cabarets continue to pay for their licenses (fixed + variable tax on the local income), governments do not seem to have enough interest to go against these businesses. Otherwise, RCI could diversify the risk of losing a license thanks to its network of 38 cabarets. The loss of an establishment would not significantly affect the group's operations.

RCI’s business model has a cyclical component. Although a decrease in consumption is not expected for the next few years, the loss of purchasing power of customers would decrease the frequency of attendance at cabarets and reduce the average ticket per capita. Besides, the industry does not enjoy the tailwinds from the 80s and 90s anymore. The customer base that has been frequenting the same cabarets for years will end up giving way to a generation Z that admits not having as much interest. New platforms like OnlyFans might not replace the cabaret experience, but they could take away their share. The consumer is finding added value on the internet and the unit economics of these platforms for dancers are significantly higher. There are 26 million subscribers in OnlyFans alone and the platform charges 20% to content creators.

I don’t think the management is a risk but it was undoubtedly the biggest responsible for the investigations that the SEC carried out between 2019 and 2020. The behavior of the management did not measure up to a Nasdaq company, which was on the verge of being reported for their delay in the delivery of the annual accounts. Additionally, Eric Langan and his team have a tainted record for making a large acquisition that turned out to be a fraud and for diluting capital at the worst possible times. Link 1, Link 2 and Link 3 can provide more information on these topics. Eric Langan has been the CEO since he was 29 years old and acknowledges having learned his lesson. Although the human being is the only animal that trips twice on the same stone, it seems that Eric Langan, who owns 8% of the company, is the person with the most interest in not repeating the same mistakes again.

DISCLAIMER: This analysis is not an investment recommendation. The author is a shareholder since RCI Hospitality was a $200 million market cap company and his projections could be wrong. Please, do your own due diligence.