Vidrala (VID) and the European glass container industry

I think Vidrala is relatively little known among European investors, unknown among international investors and certainly undervalued by the market as a whole. Not so much for its valuation itself, but for the general perception of the strengths of its business model.

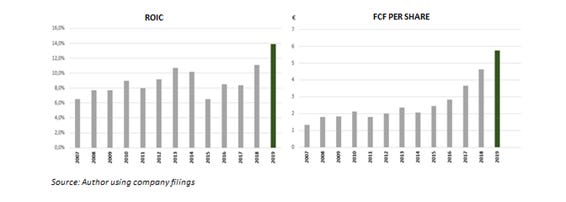

Vidrala is the third largest producer of glass containers for food and beverage products in Europe. It is a well run business and the most efficient among the four biggest players in an industry that is not excessively competitive and with moderate tailwinds (when income increases, demand increases). Vidrala has competitive advantages due to its low incremental unit cost and its unique final product, as well as the quality of the management, who place great emphasis on generating FCF over the long term and protecting a return on invested capital adequate (13.9% pre-Covid).

Vidrala is a family business, with just over 30% of the shares in hands of the CEO (the founder’s grandson) and shareholders close to the family, which operates in an oligopolistic industry, with stable revenue and high barriers to entry because of the particularities of glass.

The management’s excellent capital allocation has achieved 9% revenue CAGR and 13.4% FCF per share CAGR growth respectively since 2007. Although the management has a good track record in M&A, inorganic growth is very opportunistic. Reinvestment limitations mean that free cash flow is distributed as dividends and used to buy back shares while maintaining good discipline in capital allocation.

Brief overview of Vidrala's operations

Vidrala Group, with more than 50 years of history, is the third largest producer in Europe (15% market share) of glass containers for food and beverage products and the second most important in the Iberian Peninsula (33% market share). The Group offers customized and environmentally sustainable solutions to more than 1,600 customers from different sectors:

- 35% of revenue comes from wine packaging

- 30% comes from beer packaging

- 13% comes from food packaging

- 9% comes from liquor packaging

- 7% comes from packaging for champagne, juices and water

- The remaining 6% comes from soft drink packaging

The solidity of Vidrala's business model is sustained thanks to its international industrial network (presence in more than 5 countries, with more than 19 furnaces spread over 8 production centers and more than 3,700 employees) together with an excellent relationship with small and large customers built over the years.

At the end of 2020, the group's geographical revenue was distributed as follows: Spain and Portugal (39% of revenue), United Kingdom and Ireland (36%), Italy (7%) and the rest of Europe (18%) . Thanks to its international presence, customers receive a better service (in terms of adaptability and delivery times) and transport costs and working capital needs are reduced.

The main competitors of the group are Verallia (29% of the European market share), Oi (29%), Ardagh (13%) and regional companies with smaller scale as Vetropack, BA Vidro and Zignago Vetro (14%).

Vidrala's industry and competitive advantages

Glass and its peculiarities

Vidrala is well positioned to benefit from the secular tailwinds in the glass packaging market, driven by consumer preference for this type of material over traditional plastic packaging (lower cost packaging). The consumer is increasingly concerned and more aware of the characteristics of glass in terms of environmental sustainability (100% and infinitely recyclable material), its properties (the risk of filtration of chemicals harmful to health such as Bisphenol A is eliminated) and its ability to preserve flavors. According to an independent study from 2017, 85% of those surveyed recommended glass as the material par excellence to their families (15% more than in 2008). Of the 18,000 respondents in 11 European countries, 76% considered glass as the most environmentally sustainable material (50% more than in 2008). Governments and the European Parliament are also starting to aggressively bet on recyclable or multi-use materials such as glass and they are starting to penalize single-use packaging such as plastic with big use restrictions.

Glass is also the favorite option in branded products or “premium” products due to its differentiation or perception of exclusivity, especially in spirits (with a penetration rate close to 100% in 2018). It also stands out for its presence in sparkling wines (penetration rate close to 100% in 2018) and normal wines (close to 75% penetration in 2018) due to its image and resistance to pressure. Disruption in these products with alternative material packaging is very limited, which places Vidrala in a privileged position compared to other players (close to 50% of the Group's revenue comes from the sale of this type of bottles).

Although with lower rates (65% penetration in 2018), beer (30% of the Group's revenue) also opts for glass as its preferred material. A good part of the beer market uses glass as a differentiation tool where the brand matters as much as the taste. Penetration rate in regional or local breweries is much higher; trying to create an image that highlights the distinctive flavor of their beers compared to the largest competition.

On the other hand, the preference for glass in food products (13% of Vidrala's revenue) varies depending on the region and the category. However, the characteristics of glass (the possibility of sterilizing it or being subjected to high temperatures) make it one of the materials preferred by consumers.

A market with a local character

Today the glass industry is more efficient than ever and continues to look for ways to provide better service ($) to customers, thus strengthening its competitive position and future cash flows. Vidrala's markets are, for the most part, regional due to transportation costs. The low value of the bottles with respect to their weight and the space they take makes transporting long distances economically unfeasible. The very characteristics of glass act as a defensive pit for producers, thus limiting imports from potential international producers on a larger scale. According to 2013 figures, 90.7% of the production of glass bottles in Europe was destined for local consumption, while 9.3% of what was exported were hollow glass products of complex manufacture.

Due to the local nature of the industry, glass production centers are often located close to end customers. In the same way, production centers must be as close as possible to suppliers. Hollow glass is formed (excluding recycled glass) of silica sand (between 60 and 70%), sodium carbonate (between 10 and 20%) and limestone (15 and 20%). The cost of transporting sand and limestone with respect to the original cost of the raw material is between 4 - 5 times and 3 - 5 times, respectively. The number of suppliers is usually very small due to the limited stocks of their material sources.

All these particularities limit the existence of greater competition in the same region.

An industry marked by high technical processes, logistical difficulties and capital intensity

The hollow glass manufacturing industry requires mastery of complex technical processes as well as large capital investments. Industrial processes have a high technical component to guarantee the quality and safety of the containers that not only require qualified labor, but also constant training. For the customer, price is an equally determining factor as the security of supply, the quality and durability of the product.

The market is also significantly capital intensive. Building a plant with the capacity to produce 80,000 tons per year requires an investment of ~ $100 million (furnaces being the key investment of the project, ~ $50 million). The time elapsed until the plant can start producing is around two years. Once it’s finished, the plant needs to reach a minimum utilized capacity of 80% in order to be minimally profitable due to the high percentage of fixed costs compared to the total (60%) and the high initial investment. Plants often need high automation in their processes and operate 24 hours a day and 365 days a year to achieve certain economies of scale and obtain reasonable returns on invested capital. Achieving all this can only be feasible with a previously established customer base and a clear international / local presence. Having a broad and diversified portfolio such as Vidrala's is an especially relevant competitive advantage in a sector where customer retention rates usually exceed 80%.

Capital investments do not end with the first capital injection. IS furnaces and machines have a useful life of 10 to 12 years. Rebuilding each element can entail an investment of up to $18 million and $2,5 million. The time required to replace each item is usually around 2 to 3 months and 3 to 4 weeks respectively. The recurring maintenance capex is around 7 - 8% of the revenue. In addition, the delivery times of these materials require very demanding planning and execution. For this reason, producers tend to integrate logistics (investment in trucks and specialized machinery) as part of their services.

All these operational requirements reinforce entry barriers in an already complicated market, dominated by large players with more than 50 years of experience.

Increasingly stricter legislation

The industry is subject to European, national and local regulations in order to operate. Producers require permits and authorizations in fields related to the environment, safety and public health, such as operating permits, wastewater discharge, water extraction and authorizations for the transport and disposal of hazardous waste, which are subject to renewal, modification, suspension and possible revocation by the administration and the government.

Producers are also subject to restrictions on their carbon dioxide emissions. These restrictions are expected to increase in the coming years due to concerns about climate change. The industry will have to make a significant investment in order to adapt to new regulations, something that will particularly affect competitors with less scale.

Obtaining permits to build new plants or even expand the facilities of existing ones is increasingly complex and the process is tedious, reinforcing entry barriers and discouraging investment in increasing industry capacity.

Consolidation in a European market with favorable trends on the supply and demand side

All of these previous operational requirements reinforce the entry barriers in an already complicated sector, dominated by 4 large producers (Vidrala being the third) with more than 50 years of experience that account for more than 85% of the market. Due to the high initial investment and the complexity of building a client portfolio, companies tend to grow by M&A.

The European market has undergone a significant consolidation in the last 20 years and is currently in an oligopolistic position where competitive dynamics are not based on pricing strategies. Europe is a mature and stable market, linked to consumption, where demand has grown in the last decade at 2% per year (closely linked to GDP). Supply has been much more volatile. As 85% of the market is dominated by 4 players and the risk of breaking price dynamics would harm each of them, the trend of recent years has led to divestment and reduction of capacity. More leveraged producers such as OI, Verallia and Ardagh have led this strategy, closing 9 plants and 7 furnaces in recent years.

Privileged competitive position thanks to location

Vidrala is the third largest European producer in terms of sales, but it is still well behind giants such as OI or Verallia. Although scale matters, once the producer reaches a certain size it begins to take on less relevance or even to harm the returns on the company's invested capital (more leverage, necessity of manufacturing of larger runs to supply multinational clients, more competitive prices pressured by the power of multinationals, less capacity to serve the most profitable niches, etc.). Vidrala's strategic position in highly profitable market niches such as Italy, Spain and Portugal is one of its greatest competitive advantages compared to more widely dispersed competitors. Unlike the beer market, dominated by large multinationals, the wine and spirits market (to which Vidrala has great exposure) is characterized by having a more fragmented base of regional and local customers, with less power over the supplier and with exposure to exports that grow faster than local consumption.

Another of the Group’s unique assets is the production plant in Santos Barosa (Portugal). The plant's competitiveness and efficiency is so much higher than the industry’s average (due to the reduced cost of labor and energy) that it can increase the company's sales scope to the heart of Europe and remain price competitive.

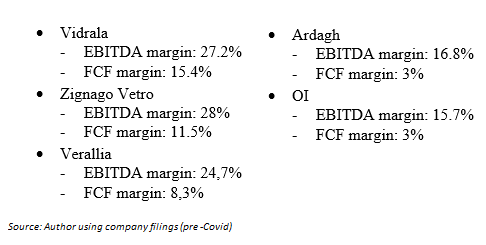

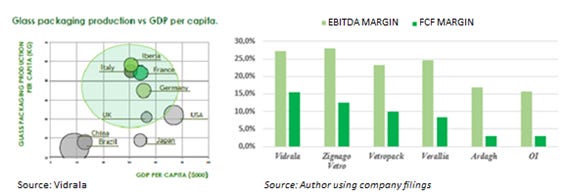

For these reasons among many others, Vidrala is the most efficient listed European manufacturer in Europe, well ahead of larger scale competitors such as OI, Verallia and Ardagh. The group's efficiency is above that of the historic family and regional company Zignago Vetro which, although it has higher EBITDA margins than Vidrala, has a higher recurring maintenance capex (11.5% of sales compared to Vidrala's 9%) due to making much shorter series of bottles and having to replace the molds more frequently.

Management

The Delclaux family founded the group in the middle of the previous century and today it is the third generation who is leading the project. Mr. Carlos Delclaux Zulueta, grandson of the founder and President since 2002, owns, together with shareholders close to the family, 30% of the Group's shares. Mr. Delclaux developed his professional career in banking and it was in 1991 when he made his first contact with Vidrala, becoming vice president of the board of directors. Since his introduction as President, Delclaux has executed a strategic plan for the expansion of the firm in which he has managed to multiply revenue by 8 through organic growth and acquisitions (never exceeding 7-8x EV / EBITDA in its acquisitions).

The management team and the board have a fixed remuneration (there are no stock options) and they are aware that the only way to see their equity increase substantially is to execute the business perfectly so that the price ends up keeping pace with the results. In his few public appearances, Delclaux acknowledges his long-term commitment, regardless of the short-term sacrifice and the importance of value creation through increased cash flows without neglecting the return on employed capital.

Industry outlook

Wine consumption in Europe is expected to remain practically unchanged until 2023 (-0.1% CAGR). To compensate for the maturity of the market, it is estimated that exports of the same products will grow at a higher level during the same period (1.7% - 2% CAGR in terms of volume). Vidrala benefits from a growing demand in emerging countries through the export of the final product (wines and spirits).

In wines and spirits of high quality or perceived by the consumer as premium, growth is expected until 2023 to be explosive (6.2% and 7.8% respectively) thanks to a strong demand from countries such as China, the USA and emerging countries compared to the 2.5% CAGR growth of less exclusive spirits. Brand or premium wines and spirits enjoy a more inelastic demand and the consumer sees the packaging as a fundamental element of the final product. Vidrala's EBITDA margins on these products are much higher than those achieved on standard products.

The glass container manufacturing market registered a growth in sales volume of 1.8% CAGR until the beginning of 2019, reaching 20.4 million tons sold. Very similar growth (1.6% CAGR) is expected until 2023, in line with global development.

Regarding inorganic growth, Vidrala is in an advantageous position compared to much more leveraged competitors (Ardagh with 4.8x net debt / EBITDA, OI with 4.5x net debt / EBITDA and Verallia 2x net debt / EBITDA) to continue with its market consolidation through small and medium acquisitions. There are still more than 50 regional companies accounting for 14% of the market that can be a target for purchase. With 0.8x net debt / EBITDA (lowest level in the last 5 years) the group is in a strong position to continue growing around Europe through M&A.

Vidrala will invest around $600 million over the next few years to increase the capacity of some of the plants but, above all, to make them more efficient. The Group's activities are electro-intensive (mainly in natural gas and electricity) since the furnaces have to operate at temperatures higher than 2.700º F for 24 hours and 365 days. 60 - 70% of the energy consumed is used in the ovens. Energy costs represent around 18% of a plant's revenue. It requires demanding production planning and rigorous management of the combustion process, monitoring of the melting process and up-to-date maintenance of the furnaces. Reducing energy consumption per ton of production is vital to achieve economies of scale and to be able to provide a more attractive customer service ($). During the last financial year, internal energy audits have been carried out to monitor energy consumption, heat recovery projects have been developed in four of its eight plants, a photovoltaic installation has been built in Portugal and old furnaces have been renovated for some more energy efficient.

The cost of raw materials and consumables needed to make glass represented 32% of Vidrala's revenues. Aware of the limitations to increase the production of the plants, the control of fixed costs is a priority objective. In recent years, investments have been intensified to reduce the consumption of main and auxiliary raw materials per ton of production and the Group's management announced that it will continue with this dynamic in the coming years.

Most notable risks

New investments in the industry

The sustainability of the returns on capital employed from the manufacturing industry, and more specifically from Vidrala, indirectly depends on the balance between demand and production capacity. Although heavy investments to increase supply would hurt all members, there is no guarantee that expansion strategies of this type will not be implemented again. This is a particularly relevant risk in an industry with a high fixed component on total costs and a pronounced difficulty in transferring excess capacity from one market to another.

Export tariffs

A high percentage of the sales of peninsular and Italian customers are due to exports, which has positively influenced the Group's revenue throughout its history. The cost of exports depends largely on trade tariffs between the country of origin and destination. Any commercial war between markets could lead to a drastic drop in exports that would end up having an impact on Vidrala's accounts.

An increase in customs fees could also affect the type of material used to transport the final product, glass being a heavier material (and therefore more expensive to transport) than plastic or aluminum.

Alternative products

Although Vidrala is one of the least affected owing to its exposure to wine and spirits, it competes against companies that manufacture aluminum containers in the beer and energy drink sector; plastic containers for bottled water, energy drinks, oils and other food products; and tetra briks for the juice, milk and wine sector.

Although glass is the quintessential choice of consumers for its sustainability with the environment, there is a real risk that companies that manufacture other materials will launch an alternative product with similar properties that could disrupt the industry. Consumers' commitment to products other than glass would put significant pressure on the Group's income statement. Excess capacity would reduce the volume / prices of the sector and until there is a new balance between supply and demand, the operating leverage itself would significantly punish Vidrala's profits.

Price of raw materials

Vidrala's activities are electro intensive and energy costs represent around 18% of a plant's sales. A strong increase in energy prices would affect Vidrala's EBITDA margins and also its gross margins (the transportation costs of silica sand, limestone and recycled glass are a good part of the final cost of the raw material). Many of the contracts between the producer and the customer are subject to review within one year and do not include clauses that allow the increase in production cost to be passed in the short term.

Economic recession

A decrease in global or regional consumption derived from a decrease in purchasing power would have a negative impact on the group's activities. Although the impact is greater in occasional products such as champagne or cava, these represent a small part of Vidrala's sales. Basic or day-to-day products that use packaging produced by the Group are less affected by economic cycles (Vidrala’s revenue in 2009 just fell by 2% and operating income grew by almost 2%).

Reuse vs recycling

In Germany, when consumers buy a product, they pay some kind of security deposit that is returned to them when they deliver the original packaging. These policies encourage not only the recycling, but also reusing of packaging. Such policies could impact the group's operations if they are extended to markets where Vidrala is present.